|

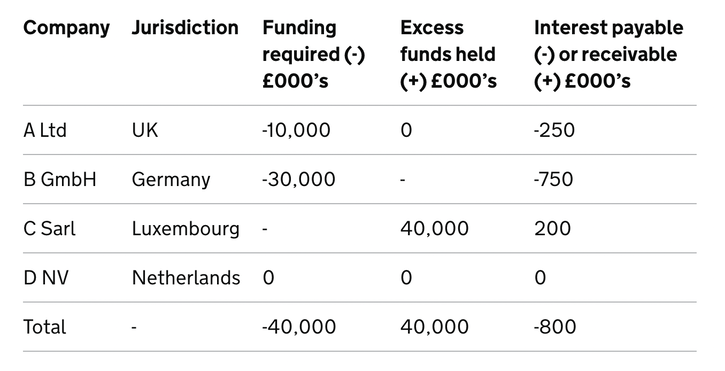

For multinational corporations, a cash pooling arrangement can save on interest payments and offer global visibility of cash. Pools are normally administered by either a treasury company or in-house bank (for larger groups, also providing a range of treasury activities) or a group finance company (for smaller groups, with activities normally limited to cash pooling and longer-term funding). The aim is to manage the group’s cash position on a consolidated basis, effectively concentrating the group’s cash in one place. These arrangements seek to maximise the return for the group as a whole on their cash, minimise the cost of funding and give visibility to the group’s cash and currency position. Cash pooling arrangements are usually set up with the help of the group’s third-party bank, often with the support of a treasury technology provider, and allow the group to net off the credit and debit positions of the individual group companies, for the purpose of calculating the net interest payable/receivable. Example A group consists of four companies, which have differing funding requirements over the period of a year, as shown in the table below. The interest rates applied to balances are as follows (likely in reality to be margins over/under the respective LIBOR rates for the specific currency, but for illustration purposes shown as fixed rates): Deposit rate (instant access) 0.5% Borrowing rate (repayable on demand) 2.5% It is assumed that these amounts do not fluctuate for 12 months.  In the example provided above, if no cash pooling arrangement is in place, the group’s net interest payable to the third party bank is £800k. However, the aggregate balance owed to the third party bank throughout the year was nil (£40 million funding required and £40 million deposited). If a cash pooling arrangement was put in place, with D NV being the cash pool header company administering the cash pool, interest would only be charged by the third party bank on the net balance, which is nil. This means that the group overall receives a benefit of £800k as a saving of external interest payable. This can also be calculated as the spread between the deposit rate and the borrowing rate (2.5%-0.5%=2%) multiplied by the balance owed (2% x £40 million = £800k), demonstrating that the spread that the third party bank would have earned on the depositing and borrowing has been enjoyed by the group. In addition to reducing the cost of external borrowing for groups by only paying interest on the net amount borrowed (i.e. by taking into account deposits made by other group companies), there are several other benefits of cash pooling for groups:

This article is based on information from HMRC (UK), reproduced and adapted under the Open Government Licence v3.0,

1 Comment

|

- Home

-

Events

-

Solution Providers

- Accesspay

- Agicap

- AtlasFX

- Bottomline

- Bureau van Dijk

- CashAnalytics

- Cobase

- ComplyAdvantage

- COUPA

- Delega

- Fides

- FinanceKey

- FXGuard

- GTreasury

- Hedgebook

- HedgeFlows

- HedgeGo

- ION Treasury

- Kantox

- Kyriba

- MillTechFX

- Nomentia

- nsKnox

- Payable

- Redbridge

- RiskScreen

- Salmon Software

- TIS

- Titan Treasury

- TreasurySpring

- Trovata

- Trustmi

- TRUSTPAIR

- Present your Solution

- Dragons Services

- News

- Resources

Adaugeo Media Ltd

Blackwell House Guildhall Yard London EC2V 5AE United Kingdom |

Tel +44 20 3086 7753

e-mail [email protected] Incorporated in England No. 7937595 VAT GB 134596790 BTW NL 824171330B01 Privacy Policy (GDPR) Terms of business © Adaugeo Media Ltd 2023

|

FSQS Level 2

Accredited |